Debt is something most of us face at some point in our lives, whether it’s from student loans, credit cards, mortgages, or personal loans. While debt is a normal part of life, managing and controlling it is vital to avoid financial stress.

What follows is a two-part guide to help you take control of your debt.

Know Your Debt

The first step to controlling your debt is knowing exactly how much you owe. Make a list of each debt, noting interest rate, minimum payments, amount left to pay, and when payments are due.

Remember debt comes in many forms, such as mortgage, car loan, student loan, WINZ advances, AfterPay, credit cards, overdraft, loans from friends and family. You may find it helpful to use a debt tracking tool or app (such as Sorted or Booster) to help.

Create a Budget

The next step is to set up a realistic budget, as this is essential to managing your debt. A budget will help you identify areas where you can cut back and free up more money to pay down your debts faster. By knowing your income and expenses, you see if you have some income you can specifically use for debt repayment.

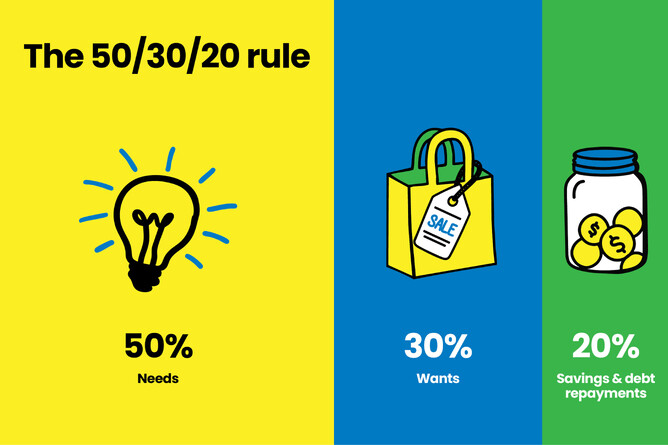

A great rule for a budget is 50/30/20 - 50% for needs, 30% for wants, and 20% for savings and debt repayment.

Focus on High-Interest Debt First

Now you know what you have available for paying off debt, it’s important to prioritise the debts with the highest interest rates, typically credit cards or payday loans. This saves you the most money overall because you’re reducing the higher interest charges first.

If you have lots of high-interest debts, pay off the one with the smallest balance first. Paying it off will be very satisfying and help you to stay motivated.

However, If you have lots of debts with varying interest rates, consolidating or refinancing will simplify your payments and potentially lower your interest rates. (Debt consolidation means combining multiple debts into a single loan, while refinancing involves taking out a new loan with better terms to pay off existing debts.)

Cut Back on Non-Essential Expenses

If you are serious about controlling your debt, this may involve making short-term sacrifices. Take a good, hard look at your spending habits and identify areas where you can cut back, such as fewer takeaways, cutting back on smokes and/or alcohol, and cancelling unused subscriptions.

Set a goal for saving a specific amount each week, and use it to repay your debt.

In Conclusion

Controlling debt isn’t about making quick fixes; it’s about creating a plan, sticking to it, and making steady progress over time. With determination, consistency, and a little bit of help when needed, you can take control of your debt and build a solid foundation for your financial future. Remember, it’s a marathon, not a sprint, but every step forward is a step toward financial freedom.

Part 2 of the guide to help you to control your debt rather than it controlling you will be next month.

In the meantime, remember – we are here to help.